Accuracy and efficiency in the reconciliation process are critical for business success. Without clear understanding of how much money the business holds can have a direct impact on cash flow decisions. Failure to reconcile transactions can lead to delays in identifying received payments or outstanding invoices. Businesses are also more likely to be affected by fraud, as it becomes difficult to detect unauthorised transactions or discrepancies in their accounts.

Understanding reconciliation match rate

When a business receives payments from customers or clients, they need to ensure that each payment can be correctly identified and associated with the specific invoice or record it corresponds to. The reconciliation match rate indicates how well a company is able to achieve this accurate matching.

The reconciliation match rate refers to the percentage of successful matches between incoming payments and corresponding invoices, orders, or customer records. It involves comparing and aligning various data points, such as invoice details, payment amounts, dates, and payment references. A high match rate means the reconciliation process is accurate and that allows businesses to close their books and prepare financial statements to understand the financial health of their business.

What is a payment reference?

A payment reference is a piece of information that is added to the transaction to help identify the purpose of the transaction. It is typically used for business payments to help match specific payments to the invoice, but when funds are sent by bank transfer, this is particularly error-prone.

If you have ever made a bank transfer, you will see the optional open text field asking for Reference. It can be as simple as a customer number or invoice number, or they can be more descriptive, such as "monthly rent" or "birthday gift”, depending on the context.

The purpose of a payment reference is to help the payee identify the payment. This is especially important for businesses that receive a large number of payments each day and use payment references to track customer payments and reconcile invoices. By including a payment reference, businesses can easily track customer payments, match the payment to the correct invoice or customer account and streamline their reconciliation process when they need to close their books.

The reality of using payment references

When making a transfer, the payer is typically asked to enter the following information:

- The recipient's name: who you are transferring the money to

- The recipient's bank details: where you are transferring the money to

- Payment reference: context about the payment

The reference field is key. It can speed up and simplify the process of identifying who sent the funds and how that money is dealt with when it is received.

Now let's see what information the payee should receive when the transfer lands in their account:

- The payer’s name: who sent the money

- The payer’s bank details: which account the money came from

- Payment reference: the identifier set by the payer

Often than not, payees don’t have access to all the information about the payment. The bank details may not be available or the name may not be present - it may be truncated or parsed in a different format. In that case, payees might also need to look for additional sources to identify where the payment came from.

So how do you allocate your money when you don’t have all the information about the payment?

You guessed it - the payment reference.

Using that reference, the window cleaners were unable to allocate the funds to the payments we had sent. They didn't have access to our bank details, they only had our name. Now imagine how many "A Smith" customers they might have on their record.

Eventually, it was all sorted and the window cleaners began instructing their customers to use specific payment references (house number, road and postcode) when sending funds. It made their reconciliation work so much easier.

The reference is that one piece of the transaction both parties have control over (let's ignore that cheques exist)! A company can define a unique reference, either for a specific customer, or a specific purpose. The customer has control over entering this reference when they create the payment. And voila! Using payment references can significantly reduce time spent matching payments with invoices.

How to encourage the use of payment references

So how can you, as a company, ensure your customers are supplying the correct reference?

Make it easy for customers to include payment reference

Human error will always happen with customers mistyping or simply not including it at all, but good UX is important to encourage input and reduce errors. Make sure that the payment reference field is easy to find and use. Depending on which payment rails are used (BACS in the UK or SEPA in Europe) , there can be character format or length limitations that can affect reference field.

Educate the payer about the benefits of payment reference

Ensure your customer understands the importance of matching the payments with their account to keep their balance accurate. Payment references also can be used as evidence in case something needs to be disputed. If you see payments coming in without a reference, send your customers a gentle reminder and explain why it’s important to include them.

Pre-fill payment reference when requesting the payment

Using Open Banking payment initiation, or a payment service provider such as Stripe, or Checkout for payment collection gives your company complete control in setting the reference for the transaction. In that way, you don’t need to rely on the payer setting the reference and you can eliminate human error and streamline your matching process when reconciling.

In summary

While it might seem like a small detail, payment references can significantly disrupt your financial operations and how much time is spent on locating, matching and reconciling the payment with the correct invoice. It's upside is that it can increase your customer satisfaction with your business if you keep all your books in order and customer accounts in check. Payment references on their own won’t solve all your reconciliation challenges, but they play an important, if not the most important, part in allocating funds efficiently and reducing time spent on manual reconciliation.

Announcements

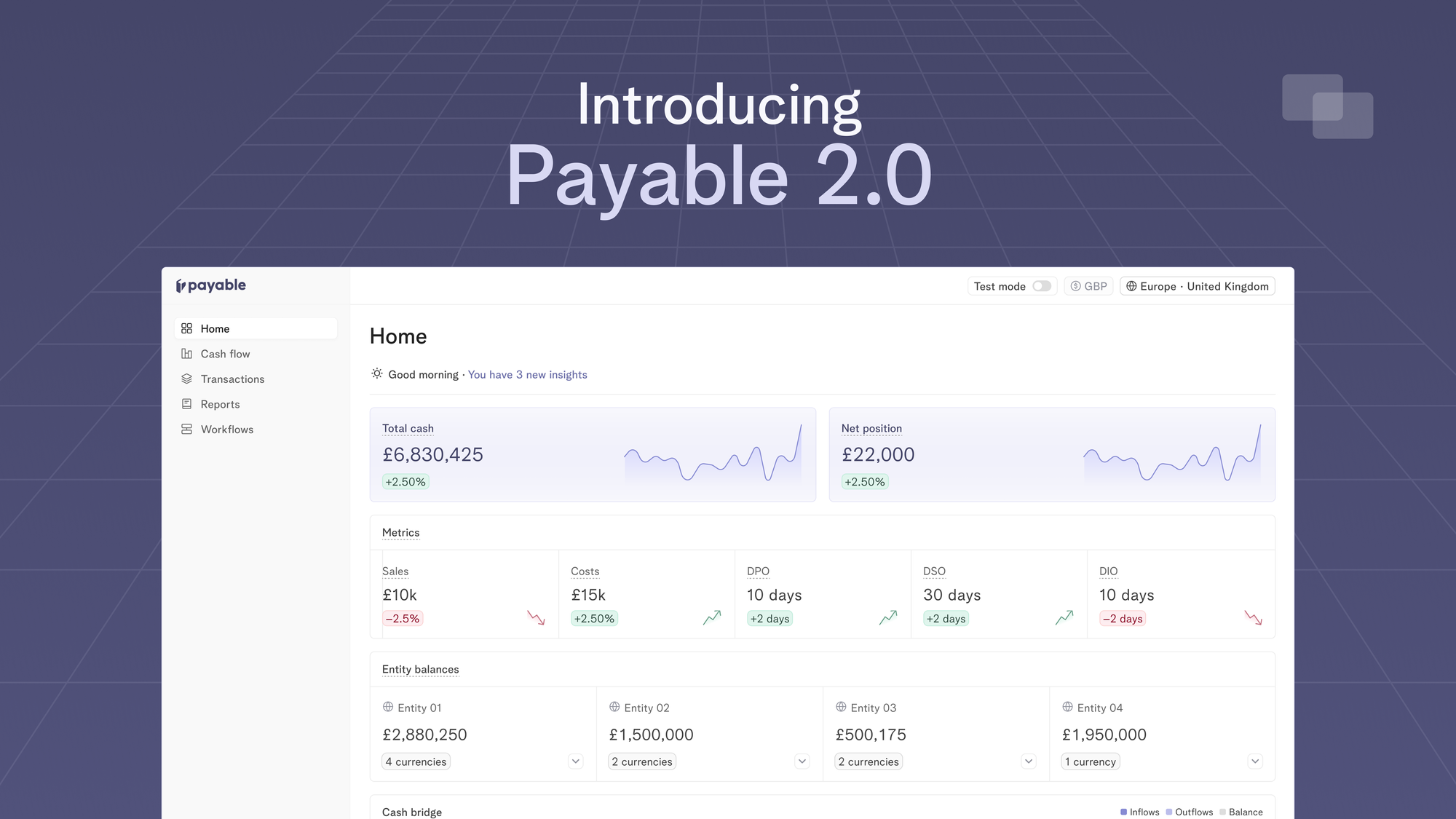

Introducing Payable 2.0 - one platform to optimise working capital, make fast liquidity decisions and move your cash metrics in real-time

13 Apr 2024

Today, we’re excited to launch Payable 2.0 which is our evolution to a more connected, intelligent and automated platform for finance teams to track their cash flows in real-time.

Cash Management

Mastering 13-week direct cash flow forecasts

26 Mar 2024

Knowing how your cash flow will behave in the future is crucial for the success and sustainability of any company. One way to achieve this is through the use of a 13-week direct cash flow forecast, which provides a detailed projection of a company's inflows and outflows over a specific time period.