In the digital age, there are new ways to connect with banks and access their services. Old-school methods like paper transactions and manual work have given way to more efficient, automated solutions. Bank connectivity keeps the money moving and lets companies pay their bills, get paid, and do all their financial tasks more efficiently. We’ll break down and compare four common bank connectivity options: Host-to-Host, EBICS, APIs, and Open Banking. We'll dive into what each option brings to the table without the corporate jargon.

Host-to-Host Connectivity

Host-to-Host (H2H) connectivity is a direct and secure way for a company to send financial data back and forth with a bank. Think of it as a private data highway between them. It typically involves the use of a dedicated leased SFTP connection and IP whitelisting.

Here are some key points to consider:

- Security: H2H is very secure. Data goes directly between the company and the bank, no detours. It uses encryption and authentication to keep data private.

- Speed: It is generally slower, as you get data in ISO files daily or on an intra-day basis, rather than in real time.

- Customisation: H2H allows for tailor-made data exchange, bending to fit any business needs.

- Implementation: Setting up H2H needs tech know-how and teamwork between the company and the bank.

- Costs: It can be a bit pricey to cover upfront costs and ongoing maintenance. And these costs would differ from bank to bank.

EBICS (Electronic Banking Internet Communication Standard)

EBICS is a standard way to exchange data with banks online, predominantly used in Germany, Austria, Switzerland and France.

Here are the key takeaways:

- Security: EBICS is all about keeping things secure. It uses encryption and digital signatures to lock down the data.

- Multi-banking: EBICS allows companies to connect with multiple banks using a single protocol. It's like connecting with multiple banks using a single remote control. Easy and efficient.

- Functionality: EBICS supports a wide range of financial transactions, including payments, collections, and reporting. It provides extensive control and monitoring capabilities for managing banking activities.

- Standardisation: EBICS uses the same language across different banks and software. So, no translation issues. This simplifies integration when using multiple banking partners.

- Implementation: Implementing EBICS needs the right software and coordination with the bank. It may involve initial setup costs and ongoing maintenance, depending on the chosen software provider.

Proprietary API (Application Programming Interface)

APIs are a set of protocols and tools that allow different software applications to communicate with each other. In the banking context, APIs are built by the bank to allow access to their banking services programmatically. Bank APIs will not necessarily conform to a set standard, but will often use ISO 20022 for sending and receiving messages.

Here's what you need to know:

- Flexibility: APIs provide a flexible and scalable solution for integrating banking services into company systems or applications. They're fast and let you do things in real-time.

- Speed and efficiency: APIs make data exchange quick and efficient. You get to make decisions on the fly and keep your customers happy.

- Security: APIs come with safety features like authentication and authorisation. Your data is locked up tight and in compliance with industry standards, such as OAuth 2.0.

- Implementation: Implementing APIs requires development resources and technical expertise. Banks typically provide documentation and developer support to facilitate integration efforts.

- Costs: Similar to H2H connectivity there are upfront costs and ongoing maintenance fees to keep in mind.

Open Banking

Open Banking is a regulatory initiative that is all about letting customers share their financial data securely with other licensed providers.

Here's the lowdown:

- Control: Open Banking gives customers the power to share their financial data with approved providers. This leads to personalised services and better money management.

- Enhanced services: Open Banking encourages teamwork between banks and fintech companies. Customers can enjoy services like account aggregation, budgeting tools, and loan comparison platforms.

- Security and privacy: Open Banking relies on secure APIs and strong customer authentication to ensure the privacy and protection of financial data.

- Standardisation: Open Banking typically sticks to the same standard (although some differences do exist), so different banks and providers can play nice.

- Implementation: Open Banking requires compliance with regulatory requirements and the development of secure and robust APIs.

- Scope: Banks are required to provide API access to customer data as part of Open Banking regulations, however, it is only mandatory for retail bank accounts not businesses.

Remember, not all banks offer all these choices, and what you pick depends on your needs. For example, H2H is great for security and customisation, but it's tech-heavy. EBICS is standard in some banks in Europe, but may not be available elsewhere. APIs and Open Banking offer flexibility and innovation but need some special tech know-how. Knowing what each option offers helps you make the right call and get the most out of modern bank connections for your business.

How can Payable help?

At Payable we aggregate all the different formats into a single Payable Schema, so you do not have to waste time and resources building connectivity in house. We map our own schema to the bank and payment providers, so no matter how many banks you have or if your bank connectivity is done through ISO, MT formats, EBICS or a proprietary API, Payable will do the hard work of mapping all the data, and you can simply see your balances, transactions and make payments in real time in a single dashboard.

Announcements

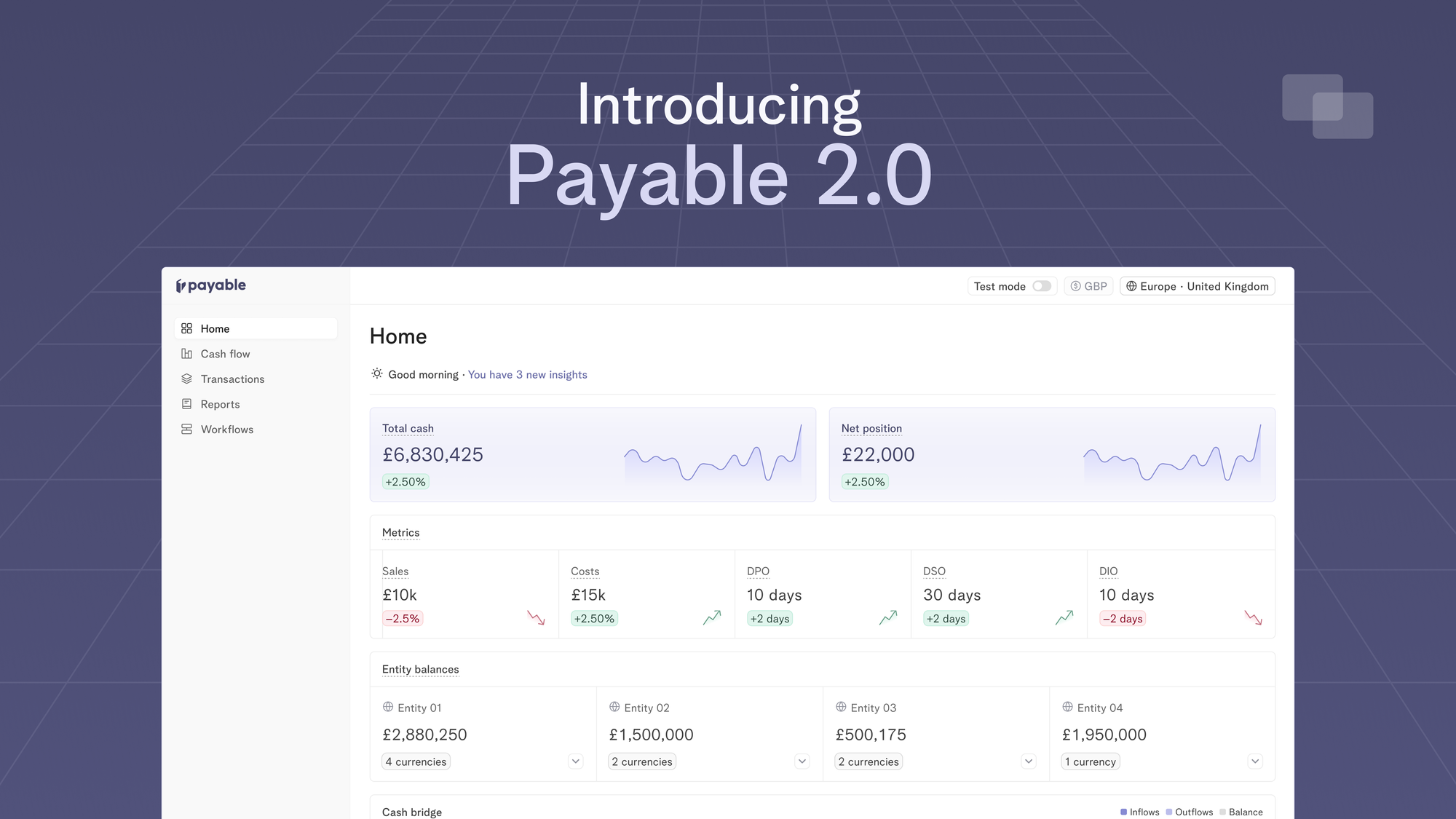

Introducing Payable 2.0 - one platform to optimise working capital, make fast liquidity decisions and move your cash metrics in real-time

13 Apr 2024

Today, we’re excited to launch Payable 2.0 which is our evolution to a more connected, intelligent and automated platform for finance teams to track their cash flows in real-time.

Cash Management

Mastering 13-week direct cash flow forecasts

26 Mar 2024

Knowing how your cash flow will behave in the future is crucial for the success and sustainability of any company. One way to achieve this is through the use of a 13-week direct cash flow forecast, which provides a detailed projection of a company's inflows and outflows over a specific time period.